Is Zomedica the Future of Companion Animal Healthcare?

A Deep Dive into Zomedica’s Business, Market Position, and Investment Case. The Risks and Rewards in the High-Growth Veterinary Health Sector. ($ZOM)(NYSE).

Trifusion AI Comprehensive Stock Analysis Report. Zomedica Corp. Ticker: ZOM (NYSE) Date: November 20, 2024 Current Price: $0.1260 (-0.79%) Volume: 3.55M shares. Market Capitalization 123.47 Million. USD.

“The global pet care market, valued at $150 billion in 2023, is projected to grow at a CAGR of 7%.”

Zomedica Corp. (NYSE Arca: ZOM) is carving out a niche in the burgeoning veterinary health sector by addressing a critical need for faster, more accurate diagnostics and therapeutic solutions for companion animals. Anchored by its flagship product, TRUFORMA, a cutting-edge point-of-care diagnostic platform, Zomedica empowers veterinarians with tools that streamline workflows and enhance decision-making.

Its TRUFORMA biosensor platform is designed to assist practitioners in the diagnosis of complex conditions. The company was founded by Gerald L. Solensky. on January 7, 2013, and is headquartered in Ann Arbor, MI, USA.

Setting the Scene.

Zomedica Corp. is a veterinary health company focused on developing diagnostics and therapeutic solutions for companion animals. Its flagship product, TRUFORMA, is a point-of-care diagnostic platform that supports veterinarians in achieving faster and more accurate results.

Complemented by strategic acquisitions like PulseVet and Assisi Loop, Zomedica has diversified its portfolio to include therapeutic devices for pain management and orthopaedic care, further solidifying its position in a market fueled by rising pet ownership and increasing healthcare spending per pet.

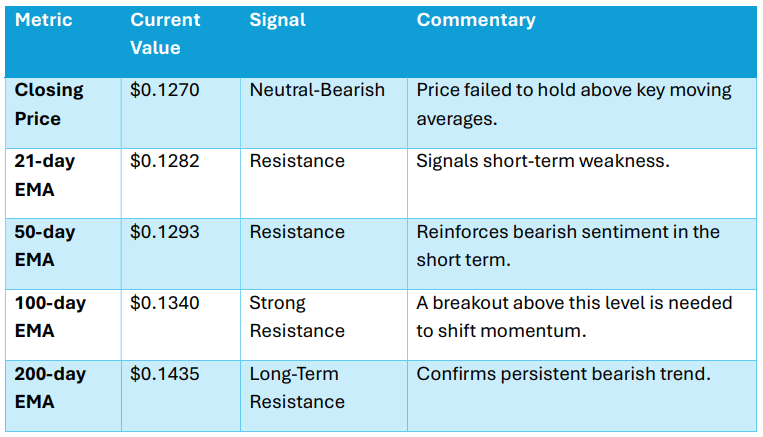

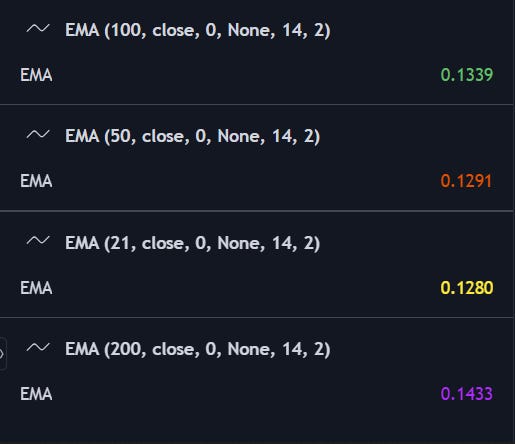

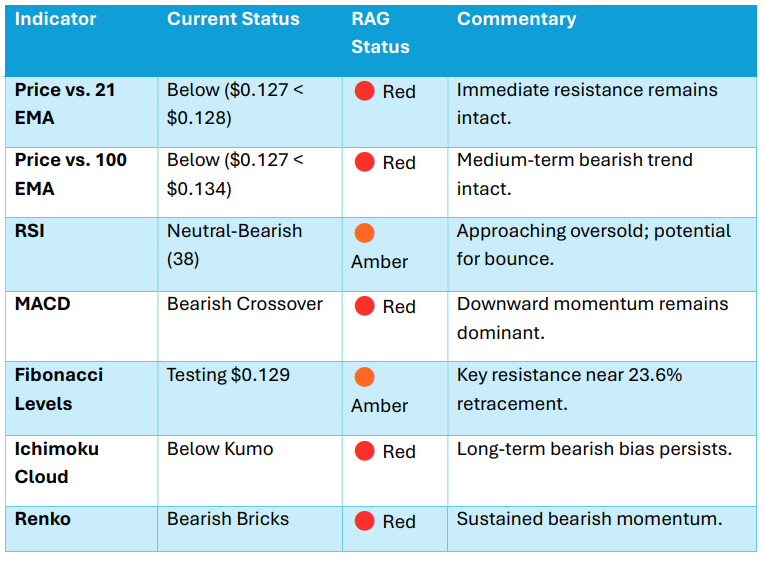

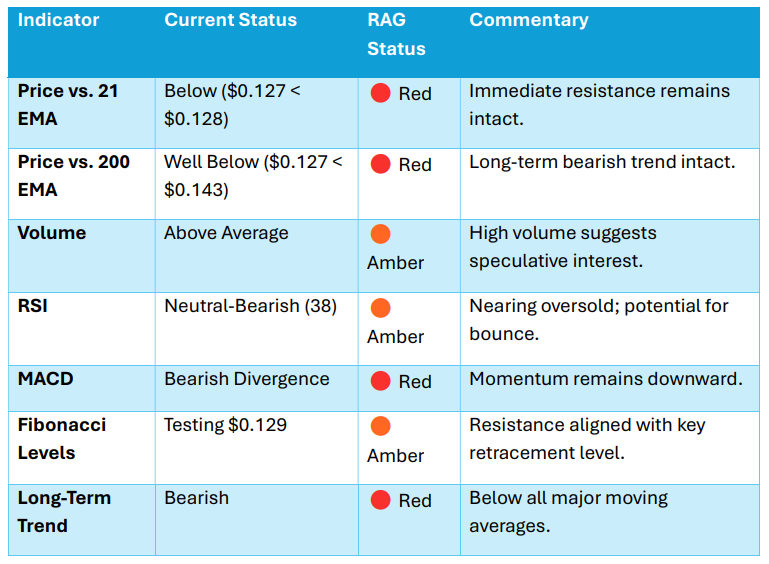

The stock has been in a long-term downtrend, consistently making lower highs and lower lows. However, recent price action shows signs of consolidation near critical support levels, supported by increasing volume. The potential for a reversal or breakdown hinges on key resistance and support zones.

“A breakout above $0.14 is needed to shift medium-term sentiment to neutral.”

Key Drivers.

Sector Tailwinds: The global pet care market, valued at $150 billion in 2023, is projected to grow at a CAGR of 7%, fueled by increasing pet ownership and rising spending on veterinary care.

Product Focus: TRUFORMA is positioned to disrupt the market for veterinary diagnostics, but adoption has been slower than anticipated.

Recent Price Action: The stock saw a sharp volume spike last week, signalling renewed interest, but it failed to sustain gains above the 200-day EMA.

Stream our Audio Podcast on Zomedica. 15-minute Must-Listen

“High trading activity between $0.12 and $0.14 indicates a critical battleground zone for bulls and bears.”

Ultimate Technical Analysis: Zomedica Corp. (ZOM)

This Ultimate Technical Analysis synthesizes multiple advanced methodologies, including Western and Eastern technical indicators, candlestick patterns, Ichimoku Cloud, Fibonacci retracement, momentum indicators, and volume analysis, to deliver an exhaustive evaluation of Zomedica Corp.’s (ZOM) technical landscape. The stock is currently exhibiting mixed signals, oscillating between key support and resistance levels, with the potential for both breakdowns and recoveries.

Price and Moving Averages.

Key Takeaways:

Price is below all major EMAs, signalling bearish momentum across short, medium, and long timeframes.

The cluster of moving averages near $0.128-$0.134 creates a consolidation zone, which the price must break out of to signal the next major move.

Volume Analysis.

Volume Trends:

Current Volume: 7.89M (above the 10-day average of ~3.5M).

Signal: Elevated volume during recent rallies indicates speculative interest but was followed by selling pressure, highlighting profit-taking or distribution.

Accumulation/Distribution (A/D) Line:

A divergence between rising A/D levels and falling prices suggests early accumulation by institutional or value-oriented traders.

Volume by Price:

High trading activity between $0.12 and $0.14 indicates a critical battleground zone for bulls and bears.

Recent Patterns:

False Breakout: Last week’s price spike above $0.14 was unsustainable, highlighting a lack of bullish follow-through.

Potential Doji Cluster: Recent small-bodied candles around $0.12-$0.13 indicate indecision, which could resolve into a significant move in either direction.

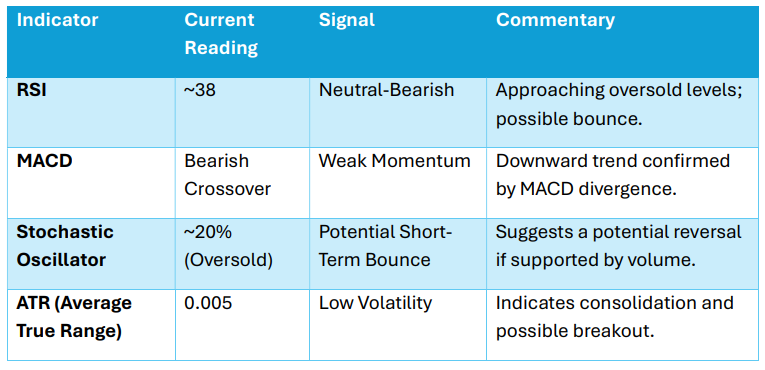

Momentum Indicators.

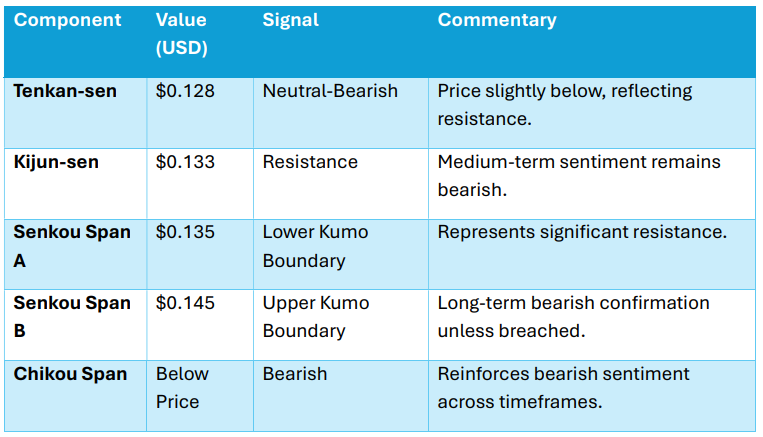

Ichimoku Kinko Hyo Analysis.

Ichimoku Insights:

Price remains below the Kumo (cloud), signalling a bearish environment. A breakout above $0.14 is needed to shift medium-term sentiment to neutral.

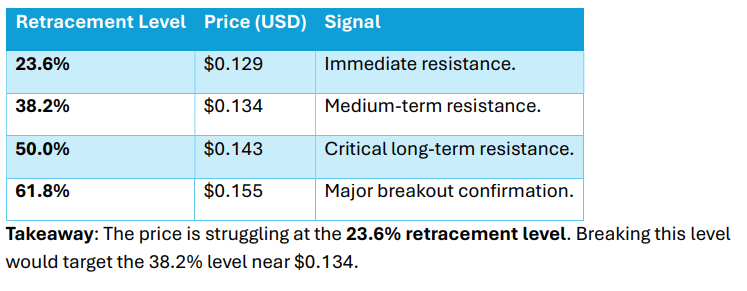

Fibonacci Retracement Analysis.

The Fibonacci retracement tool provides key levels for support and resistance:

Advanced Chart Patterns.

Descending Triangle: o Support: $0.12. Resistance: $0.14. o Implication: A breakdown below $0.12 could trigger a sharp sell-oƯ to $0.10, while a breakout above $0.14 would signal bullish momentum.

Potential Double Bottom: o Range: $0.12-$0.14. Confirmation: A breakout above $0.14 would confirm the pattern, targeting $0.16-$0.18.

Volume Spike Rejection: The recent high-volume rally and rejection near $0.14 highlight a key battleground zone.

Heikin-Ashi and Renko Analysis.

Renko Chart:

Brick Size: $0.005. Current Trend: Consecutive bearish bricks below $0.13 confirm a sustained downtrend. Key Reversal Signal: A bullish brick above $0.14 would indicate a trend shift.

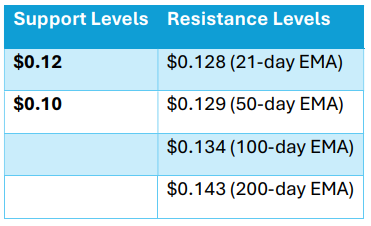

Support and Resistance Levels.

Summary Table.

Conclusion.

Zomedica Corp. (ZOM) is currently trapped in a short-term consolidation phase, oscillating between $0.12 and $0.14. The stock’s long-term bearish trend remains intact, but recent volume spikes and oversold momentum indicators suggest a potential for a short-term bounce.

“The global veterinary diagnostics market is valued at $6.5 billion (2023) and is expected to grow at a CAGR of 8% through 2030.”

Key Takeaways:

Bullish Signals: Oversold conditions on RSI and Stochastic Oscillator. Potential double bottom pattern near $0.12

Bearish Signals: Price below all major EMAs. Persistent rejections at Fibonacci retracement levels and resistance zones.

Get your FREE 'deep-dive' TriFusionAI ZOM Market Report here

Ultimate Fundamental Analysis: Zomedica Corp. (ZOM)

This Ultimate Fundamental Analysis of Zomedica Corp. (ZOM) offers a detailed assessment of its financial health, market potential, operational strengths, and risks. By delving deep into financial metrics, industry trends, and competitive positioning, this section provides a comprehensive picture for investors considering Zomedica as a speculative opportunity in the growing veterinary health market.

Business Overview.

Zomedica Corp. is a veterinary health company focused on developing and commercializing diagnostic and therapeutic solutions for companion animals. The company's flagship product, TRUFORMA, is a point-of-care diagnostic platform designed to provide veterinarians with fast, accurate, and minimally invasive testing solutions.

Core Products:

TRUFORMA: A novel diagnostic tool aimed at enhancing veterinary workflows by offering in-clinic testing capabilities.

PulseVet: Shockwave therapy for orthopaedic conditions in companion animals.

Assisi Loop: Non-invasive therapeutic solutions for pain and inflammation.

Key Markets:

Companion animal diagnostics (TRUFORMA). Therapeutic devices for pet care (PulseVet, Assisi Loop).

Industry Context:

The global veterinary diagnostics market is valued at $6.5 billion (2023) and is expected to grow at a CAGR of 8% through 2030, driven by:

Increasing pet ownership globally.

Rising awareness of companion animal health.

Advances in diagnostic and therapeutic technologies.

Join Swazers Charts FREE Telegram

Revenue and Profitability.

Key Insights:

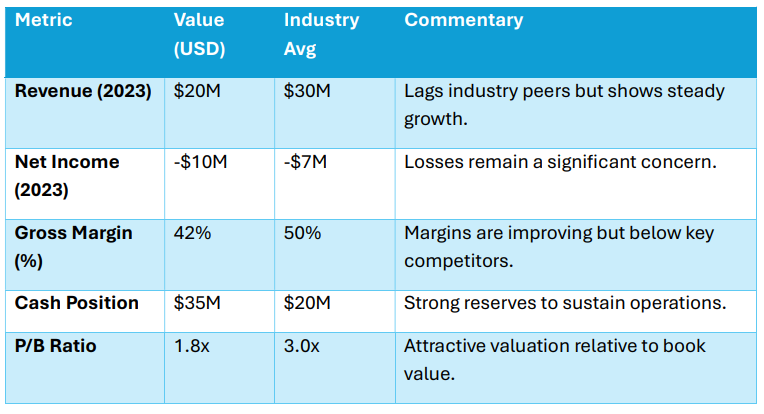

Revenue Growth: The company has consistently grown revenue by expanding TRUFORMA's product lineup and leveraging acquisitions like PulseVet.

Gross Margin Improvements: Margins have increased as Zomedica scales operations and moves toward more cost-efficient manufacturing.

Profitability Challenges: Despite narrowing losses, the company is still far from achieving net profitability, which remains a medium-term goal.

Financial Health.

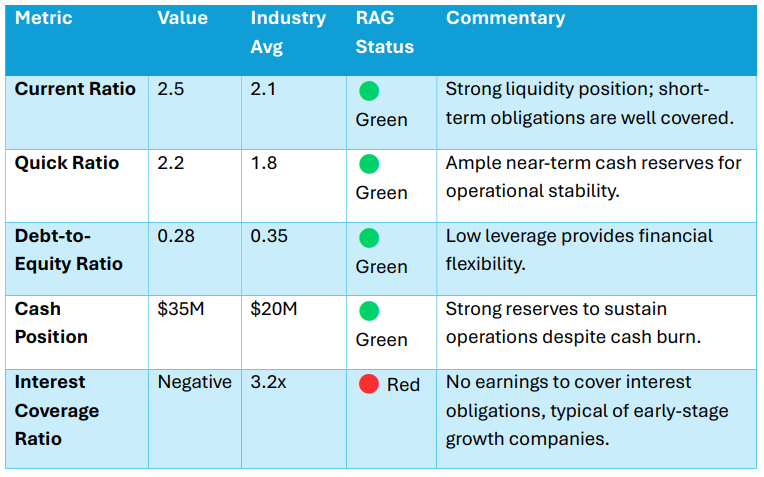

Liquidity Strengths:

Cash Reserves: With $35M in cash, Zomedica is well-positioned to fund ongoing R&D, marketing, and operational activities.

Low Debt: A debt-to-equity ratio of 0.28 ensures the company is not overly reliant on external financing.

Leverage Risks:

While debt levels are low, continued operating losses may require additional equity raises, leading to potential shareholder dilution.

Growth and Market Opportunities.

Key Drivers:

1. TRUFORMA Expansion:

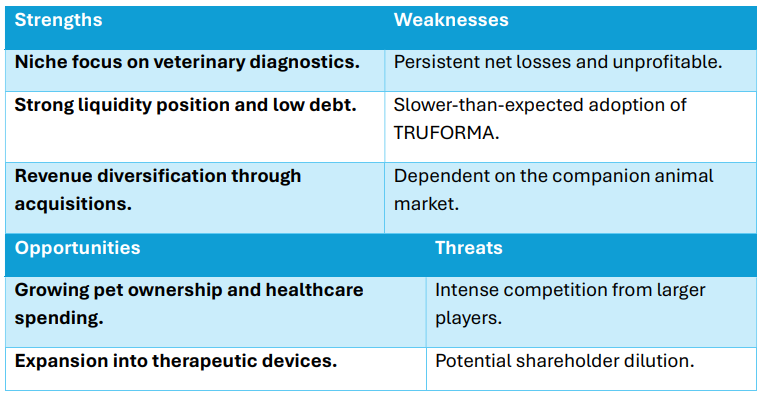

Zomedica continues to expand its TRUFORMA product line, targeting diagnostic tests for thyroid disorders, adrenal function, and other critical conditions in companion animals.

The platform’s in-clinic capabilities address a significant market need for faster and more accurate testing.

2. Acquisitions Driving Growth:

The acquisition of PulseVet and Assisi Animal Health has diversified Zomedica’s revenue streams while positioning the company in the therapeutic devices market.

3. Global Pet Ownership Trends:

Increasing pet ownership and rising healthcare spending per pet create a supportive backdrop for Zomedica’s products.

4. Regulatory Tailwinds:

Favourable regulations for veterinary diagnostics and the growing adoption of point-of-care testing further bolster the company’s growth prospects.

Competitive Landscape.

Competitive Advantages:

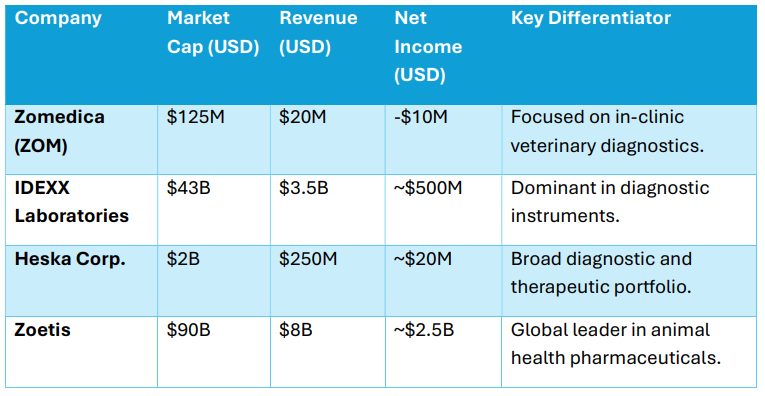

Niche Focus: Zomedica’s emphasis on veterinary diagnostics and in-clinic solutions differentiates it from larger, generalist competitors like Zoetis and IDEXX.

Small-Scale Flexibility: As a smaller player, Zomedica can adapt more quickly to emerging trends in the pet care industry.

Risks and Challenges.

1. Profitability Uncertainty:

Continued operating losses and reliance on external funding raise concerns about long-term sustainability.

2. Adoption Barriers:

TRUFORMA adoption has been slower than expected, likely due to competitive pressures and the conservative nature of veterinary practices.

3. Market Competition:

Zomedica competes with well-established players like IDEXX and Heska, which have larger R&D budgets and broader product portfolios.

4. Stock Volatility:

ZOM is a speculative stock, with significant price swings driven by retail investor sentiment rather than fundamentals.

Valuation Metrics.

SWOT Analysis.

Conclusion.

Zomedica Corp. is a high-risk, high-reward speculative play in the growing veterinary health industry. While the company’s innovative diagnostic and therapeutic solutions hold promise, profitability challenges, adoption barriers, and competitive pressures remain headwinds.

Investment Outlook:

Strengths:

Consistent revenue growth. Improving gross margins. Strong cash reserves and liquidity.

Challenges:

Negative operating cash flow.Reliance on TRUFORMA adoption for long-term success. Volatile stock price driven by speculative trading.

Zomedica is best suited for growth-oriented investors with a high-risk tolerance and a 3-5-year investment horizon. Conservative investors may prefer to wait for sustained profitability and stronger adoption metrics.

RAG Status Summary Table.

Extended Conclusion and Final Thoughts: Zomedica Corp. (ZOM)

Zomedica Corp. represents a speculative opportunity in the growing veterinary health sector, combining innovative diagnostic technologies with an expanding product portfolio. While the company's flagship TRUFORMA platform has the potential to disrupt traditional veterinary diagnostics, execution challenges, financial losses, and competitive pressures present significant hurdles. This conclusion aims to provide a well-rounded investment perspective, covering the company's appeal, risks, and strategic opportunities.

Investment Highlights (Positives)

Long-Term Growth Potential:

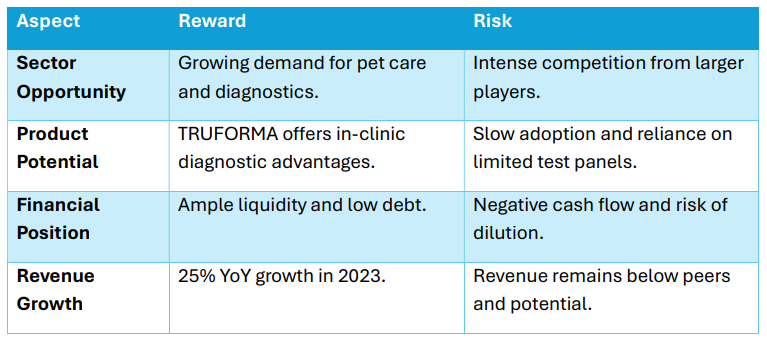

1. Veterinary Health Market Expansion:

The global veterinary health market is projected to grow at a CAGR of 7%- 8% through 2030, driven by increasing pet ownership, rising healthcare spending per pet, and growing awareness of companion animal health.

Zomedica is well-positioned to benefit from this macro trend with its diagnostics and therapeutic solutions.

2. TRUFORMA Diagnostic Platform:

Point-of-Care Diagnostics: TRUFORMA addresses a critical need for faster and more accurate diagnostic solutions in veterinary practices, enabling veterinarians to make timely decisions.

Expansion of the test panel lineup is expected to improve adoption rates and drive incremental revenue.

3. Revenue Diversification via Acquisitions:

Strategic acquisitions, such as PulseVet (shockwave therapy) and Assisi Animal Health (pain and inflammation therapies), have diversified Zomedica’s revenue streams while reducing dependence on TRUFORMA alone.

These acquisitions provide exposure to the high-growth therapeutic device market.

4. Strong Liquidity and Low Debt:

With $35M in cash reserves and minimal debt (debt-to-equity ratio of 0.28), Zomedica has the financial flexibility to sustain operations, invest in R&D, and execute its growth strategy without immediate solvency risks.

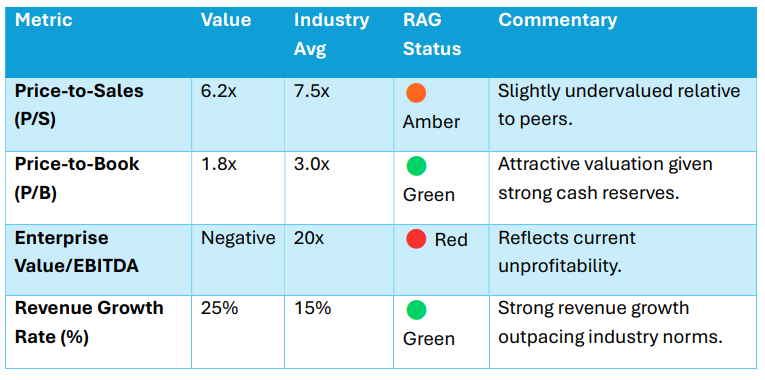

5. Valuation:

At a P/B ratio of 1.8x, Zomedica trades at an attractive valuation relative to its cash reserves and long-term growth potential.

Risks and Challenges.

Financial Challenges:

1. Profitability Concerns:

Zomedica remains unprofitable, with a net loss of $10M in 2023 and negative operating cash flow (-$6M). Achieving break-even will likely take 3-5 years.

While gross margins have improved (42% in 2023), they remain below industry leaders like IDEXX (~55%).

2. Capital Requirements:

Continued reliance on external funding could lead to shareholder dilution, particularly if cash burn persists beyond current projections.

Operational and Market Risks:

1. TRUFORMA Adoption:

The slower-than-expected adoption of TRUFORMA reflects challenges in convincing veterinarians to switch from established diagnostic methods.

Competitive products from larger players, such as IDEXX, offer broader test panels and better market penetration.

2. Reliance on Companion Animal Market:

Zomedica's focus on companion animals ties its fortunes to the growth and stability of the pet care industry. Any downturns in pet ownership trends or spending habits could impact its financial performance.

Competitive Pressures:

Zomedica competes against well-established players like IDEXX Laboratories, Heska Corp., and Zoetis, which have larger R&D budgets, global distribution networks, and established brand equity.

Pricing pressure from these dominant players may limit Zomedica's ability to scale TRUFORMA profitably.

Execution Risks:

Integration of acquisitions like PulseVet and Assisi Animal Health into Zomedica’s operations carries risks related to cost synergies and product alignment.

Key Metrics Summary.

Risk-Reward Profile.

Strategic Recommendations.

Investment Thesis: Zomedica’s long-term value lies in its ability to scale TRUFORMA adoption and expand its product portfolio through PulseVet and Assisi Loop.

Entry Strategy: Accumulate shares on dips near key support levels, targeting a 3- 5-year investment horizon for returns.

Final Assessment.

Zomedica Corp. is a speculative bet on the growing veterinary health market, offering long-term growth potential alongside significant risks. The company’s success depends on:

Scaling TRUFORMA’s adoption in veterinary clinics.

Leveraging acquisitions to diversify revenue and improve profitability.

Maintaining financial discipline to minimize dilution risks.

Overall Sentiment:

1. Bullish Case:

Strong liquidity and revenue growth provide a foundation for scaling operations. Expansion into therapeutic devices reduces reliance on diagnostics alone.

2. Bearish Case:

Continued operating losses and slow product adoption highlight execution risks. Competition from larger players limits pricing and market penetration.

Zomedica is suitable for growth-focused investors with a high-risk tolerance and patience for long-term outcomes. Speculative traders can capitalize on short-term technical opportunities, while risk-averse investors may prefer to wait for clearer profitability milestones.

"The greatest fortunes are built by patiently holding strong convictions during times of uncertainty."

#TriFusionAI © 2024 Bob Smith and John Swarbrick Follow us on X @BobSmithMSc and @SwazersC Disclaimer: This report is for educational purposes only and does not constitute financial advice.