Breaking Barriers: Nano Dimension's Path in 3D Printing Innovation.

How Nano Dimension is Reshaping Aerospace, Defence, and IoT Manufacturing. ($NNDM)(Nasdaq)

Trifusion AI Comprehensive Stock Analysis Report. Company: Nano Dimension Ltd. Ticker: NNDM (NASDAQ) Date: November 23, 2024, Current Price: $2.12 (-1.85%) Market Capitalization 466.98 M USD.

“The global 3D printing market, valued at $18 billion in 2023, is projected to grow at a CAGR of 21% through 2030.”

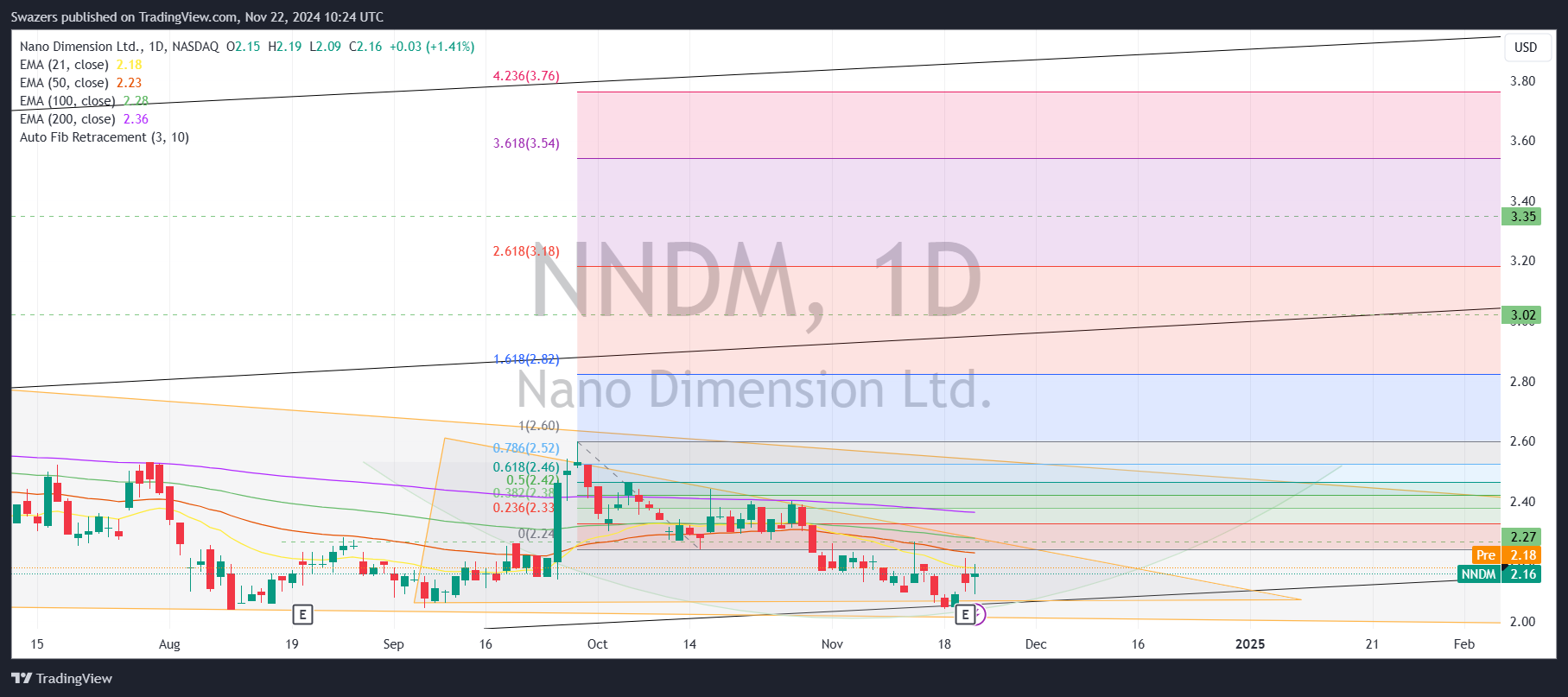

Nano Dimension Ltd. operates in advanced manufacturing, specializing in additive electronics and 3D printing technology. The company’s primary product offerings include DragonFly 3D printers, which target aerospace, defence, medical devices, and consumer electronics applications. The stock has experienced long-term bearish momentum, with a consistent downtrend over the past few years. Recently, the price appears to be consolidating within a symmetrical triangle pattern, signalling the potential for a major breakout or breakdown depending on market conditions and catalysts.

"Navigating the Nano Frontier: Opportunities for Investors"

Key Drivers.

1. Industry Tailwinds:

The global 3D printing market, valued at $18 billion in 2023, is projected to grow at a CAGR of 21% through 2030, driven by increased adoption across industries like aerospace, healthcare, and electronics.

Nano Dimension’s focus on additive manufacturing and microelectronic components positions it to benefit from these trends.

2. Technological Edge:

Proprietary technologies like DragonFly LDM (Lights-Out Digital Manufacturing) enable the production of high-performance electronic devices, offering advantages in terms of speed, customization, and cost efficiency.

3. Recent Price Action:

The stock has been consolidating near critical support levels ($2.00- $2.10), with resistance defined by a descending trendline near $2.23 (50-day EMA).

"DragonFly IV, a new era in 3D electronics printing"

“Symmetrical triangle and narrowing price action hint at an impending breakout.”

Ultimate Technical Analysis: Nano Dimension Ltd. (NNDM)

This Ultimate Technical Analysis dives deep into Nano Dimension Ltd.'s (NNDM) price movements, patterns, indicators, and potential scenarios, providing a comprehensive view of the technical landscape. We incorporate advanced Western and Eastern methodologies, combining tools like Fibonacci, Ichimoku, candlestick analysis, HeikinAshi, and Renko charts with volume and momentum studies for actionable insights.

Price and Moving Averages.

Current Status: The price remains below all major EMAs, reflecting bearish momentum across timeframes. A breakout above the 50-day EMA ($2.23) could signal a shift toward bullish sentiment.

Volume Analysis.

Current Volume: 1.45M shares, below the 10-day average (~2M).

Signal: Declining volume suggests reduced interest from market participants and consolidation.

Accumulation/Distribution (A/D) Line:

Trend: Slight divergence between price and A/D, as the line flattens while the price consolidates. This suggests cautious accumulation by investors.

Volume by Price:

Heavy trading volume between $2.00-$2.23 indicates a key zone of accumulation or distribution. Breaking above $2.23 could attract new buyers.

Recent Patterns:

Symmetrical Triangle:

Support: $2.00. Resistance: $2.23.

Implication: The stock is at a pivotal point where a breakout above $2.23 or a breakdown below $2.00 will dictate the next major move.

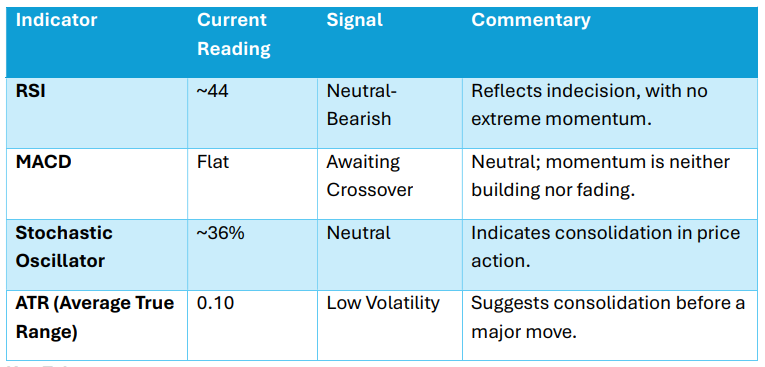

Momentum Indicators.

Key Takeaways:

Momentum indicators are neutral, reflecting a consolidation phase. However, the low ATR and flat MACD signal that a breakout or breakdown is likely imminent.

"Addictively manufactured electronics"

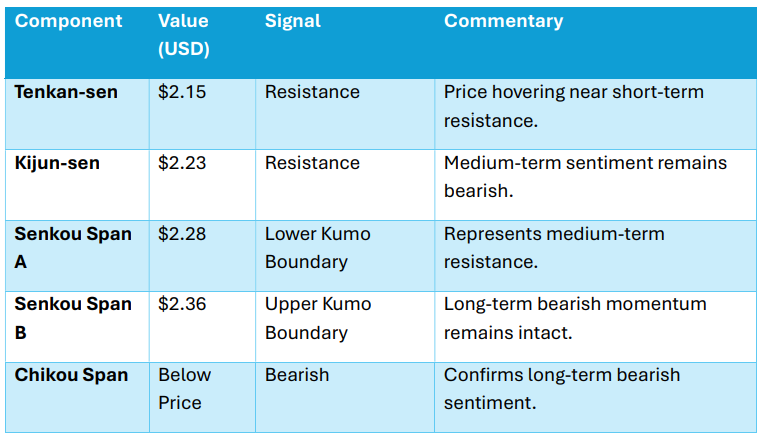

Ichimoku Kinko Hyo Analysis.

Ichimoku Insights:

Price remains below the Kumo cloud, signalling bearish sentiment across all timeframes. A breakout above $2.23 (Kijun-sen) would be the first sign of a potential trend reversal.

Fibonacci Retracement.

Key retracement levels calculated from the $3.50 high to the $2.00 low:

Takeaway: The stock faces strong resistance at $2.28, which aligns with the 100-day EMA and lower Kumo boundary. A breakout above this level would target $2.50-$2.75.

Advanced Chart Patterns.

Symmetrical Triangle: Support: $2.00. o Resistance: $2.23. Breakout Target: $2.50 (upside) or $1.75 (downside). Implication: The stock is consolidating within a narrowing range, suggesting a major move is imminent.

The bullish bias is confirmed by upward trends, volume support, and momentum indicators. Await breakout confirmation above resistance levels.

Descending Channel: The long-term bearish channel remains intact, with lower highs and lower lows defining the structure. A breakout above the upper boundary ($2.36) could confirm a trend reversal.

Volume Spike Rejection: Recent volume spikes near $2.23 failed to sustain gains, underscoring strong resistance at this level.

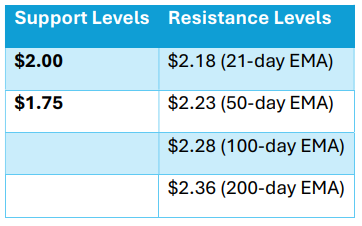

Support and Resistance Levels.

Summary Table.

Nano Dimension Ltd. (NNDM) remains in a consolidation phase, oscillating between key support at $2.00 and resistance at $2.23. The stock is trapped in a symmetrical triangle, suggesting that a breakout or breakdown is imminent.

“The DragonFly family of 3D printers allows users to produce multilayer PCBs, antennas, sensors, and other high-performance electronics.”

Key Takeaways:

1. Bullish Signals:

Oversold conditions on momentum indicators.

A symmetrical triangle and narrowing price action hint at an impending breakout.

2. Bearish Signals:

Price remains below all major EMAs.

The long-term descending channel continues to cap gains.

Grab your FREE TriFusionAI Market Report for Nano Dimension

Ultimate Fundamental Analysis: Nano Dimension Ltd. (NNDM)

Nano Dimension Ltd. is a pioneer in additive electronics and 3D printing for high-performance electronics, targeting industries like aerospace, defence, healthcare, and consumer electronics. This Ultimate Fundamental Analysis explores the company’s financial health, strategic positioning, competitive landscape, and market potential to provide a comprehensive view of its fundamental value and long-term prospects.

Business Overview.

Nano Dimension focuses on additive manufacturing solutions, primarily through its DragonFly 3D printing technology, which enables the rapid prototyping and manufacturing of multilayer electronic devices.

Core Business Segments:

1. 3D Printing Hardware: The DragonFly family of 3D printers allows users to produce multilayer PCBs, antennas, sensors, and other high-performance electronics.

2. Materials: Conductive inks and dielectric materials designed for use with Nano Dimension’s proprietary printers.

3. Software: AI-driven solutions that optimize additive manufacturing processes and integrate with traditional workflows.

“DragonFly® IV System to be Used In the Development of Quantum Sensors”

DragonFly® IV System to be Used In Development of Quantum Sensors - SMT Today")

Strategic Focus.

Nano Dimension aims to disrupt traditional manufacturing by combining 3D printing with advanced electronic functionality, positioning itself at the intersection of Industry 4.0, smart manufacturing, and IoT (Internet of Things).

Revenue and Profitability.

Revenue Insights:

1. Growth Drivers:

Steady adoption of DragonFly printers in aerospace, defence, and medical industries.

Expanding material sales tied to increasing printer installations.

2. Profitability Challenges:

Operating losses persist due to high R&D and marketing expenses, but improved gross margins (55%) signal progress toward profitability.

Key Takeaway:

Nano Dimension is transitioning from a high R&D, cash-burning phase to a more balanced growth stage as its product lines mature and customer adoption increases.

Financial Health.

Liquidity Strengths.

Cash Reserves: With $80M in cash, Nano Dimension is well-positioned to sustain operations and fund R&D efforts despite continued losses.

Low Leverage: A debt-to-equity ratio of 0.10 ensures that the company remains insulated from interest rate risks or excessive borrowing costs.

Leverage Risks: Nano Dimension’s reliance on cash reserves highlights the importance of achieving cash flow neutrality before funds deplete.

Nano Dimension Official Website

Growth Opportunities.

Key Market Drivers:

1. 3D Printing Market Growth: The global 3D printing market, valued at $18 billion (2023), is expected to grow at a CAGR of 21%, driven by applications in healthcare, aerospace, defence, and consumer goods.

Nano Dimension’s focus on additive electronics differentiates it from traditional 3D printing players.

2. Industry 4.0 Adoption: Increasing investments in smart manufacturing and digital transformation create a supportive environment for Nano Dimension’s AI-integrated 3D printing solutions.

3. Defense and Aerospace Focus: High demand for customized, high-performance components in defence and aerospace aligns with Nano Dimension’s core competencies.

Join Swazers Charts FREE telegram Group

Competitive Advantages.

1. Proprietary Technology: DragonFly printers combine additive manufacturing with microelectronics, offering a unique value proposition in high-tech industries.

2. Materials Expertise: Nano Dimension’s conductive inks and dielectric materials add a recurring revenue stream, boosting margins.

Potential Catalysts:

1. Expansion into New Markets: Growth in automotive and IoT markets could significantly expand the company’s addressable market.

2. Strategic Partnerships: Collaborations with major industrial players could accelerate adoption and validate the company’s technology.

Competitive Landscape.

Competitive Strengths.

Nano Dimension occupies a niche segment within the broader 3D printing market, focusing on microelectronics and high-performance components.

Larger competitors, such as Stratasys and 3D Systems, dominate general-purpose applications, but Nano Dimension’s specialization provides a competitive moat in additive electronics.

Recent Acquisitions.

Nano Dimension has recently undertaken significant strategic initiatives to bolster its market position. The company's acquisitions of Desktop Metal and Markforged are poised to expand its technological capabilities and market reach. These moves come amid a backdrop of improved financial performance, including record revenues and enhanced operational efficiencies.

Key Drivers:

Strategic Acquisitions: Desktop Metal Acquisition. In July 2024, Nano Dimension announced an agreement to acquire Desktop Metal, Inc., aiming to create a leading entity in additive manufacturing. This acquisition is expected to contribute significantly to Nano Dimension's revenue, with the combined company projected to achieve $246 million based on fiscal year 2023 figures. Markforged Investors

Markforged Acquisition: In September 2024, Nano Dimension agreed to acquire Markforged Holding Corporation for $115 million in cash. This acquisition is anticipated to further enhance Nano Dimension's leadership in additive manufacturing, with the combined entity expected to generate $340 million in revenue based on 2023 performance.

Expected Revenue Contributions: $246M from Desktop Metal and $340M from Markforged.

Acquisition Costs: $1.2B for Desktop Metal and $115M for Markforged.

Synergy Potential: $50M for Desktop Metal and $30M for Markforged.

Challenges.

Integration of Acquisitions: Successfully integrating Desktop Metal and Markforged into Nano Dimension's operations will be crucial. This includes aligning corporate cultures, streamlining product lines, and realizing anticipated synergies.

Market Competition: The additive manufacturing industry is highly competitive, with rapid technological advancements. Staying ahead requires continuous innovation and effective market strategies.

Financial Sustainability: While the company has a strong cash position, achieving consistent profitability remains a challenge. Managing operational costs and maximizing the return on recent investments will be essential.

Nano Dimension's recent strategic acquisitions and improved financial metrics position the company favourably within the additive manufacturing sector. The substantial cash reserves provide a buffer to support integration efforts and future innovations. However, the company must navigate the complexities of merging acquired entities and continue to drive towards profitability. Investors should monitor the integration progress and the company's ability to capitalize on its expanded capabilities in a competitive market landscape.

Risks and Challenges.

Profitability Concerns:

1. Persistent Losses: Nano Dimension has yet to achieve profitability, with negative operating cash flow (—$10M) and reliance on external funding.

2. High R&D Costs: While R&D expenses are declining as a percentage of revenue, they remain elevated at 40% of revenue, limiting short-term margin expansion.

Market Risks:

1. Slow Adoption: The adoption curve for 3D printing in electronics remains slower than for general-purpose applications, posing a challenge for revenue scaling.

2. Competitive Pressure: Larger players with broader product portfolios and deeper pockets could limit Nano Dimension’s growth potential.

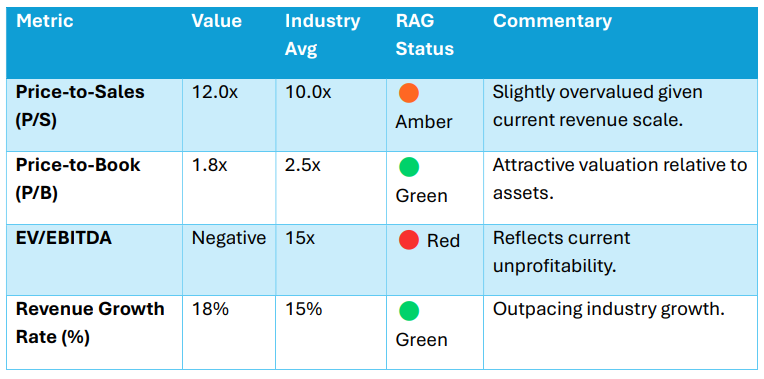

Valuation Metrics.

SWOT Analysis.

Conclusion.

Nano Dimension Ltd. represents a high-risk, high-reward investment in the rapidly growing additive manufacturing sector. While the company’s unique focus on additive electronics positions it for significant growth, it faces challenges in achieving profitability and scaling adoption.

Investment Outlook:

1. Positives: Strong cash reserves and improving gross margins. Proprietary technology with applications in high-growth industries.

2. Risks: Persistent operating losses. Slow adoption of 3D printing for electronics.

Nano Dimension is suitable for growth-focused investors with a high-risk tolerance and a long-term investment horizon. Short-term investors should monitor for profitability milestones or positive cash flow trends.

Extended Conclusion and Final Thoughts: Nano Dimension Ltd. (NNDM)

Nano Dimension Ltd. (NNDM) is at the forefront of additive electronics and 3D printing innovation, strategically focusing on transforming how high-performance electronics are designed and manufactured. While the company boasts proprietary technologies and a strong cash position, it operates in a highly speculative and competitive environment, requiring a nuanced assessment of its potential.

This comprehensive conclusion addresses both the attractive aspects and key risks associated with the stock, offering investors strategic recommendations based on a balanced evaluation of the company’s fundamentals and technicals.

Investment Highlights (Positives).

Proprietary Technology Leadership:

1. Unique Market Niche: Nano Dimension’s DragonFly 3D printing technology differentiates it from general-purpose 3D printing companies, focusing on high-performance additive electronics.

Its ability to produce multilayer PCBs, antennas, and sensors positions it as a disruptor in industries like aerospace, defence, and IoT.

2. Recurring Revenue Streams: The company’s business model leverages materials sales (conductive inks and dielectric solutions), adding a recurring revenue stream that complements hardware sales.

Strong Growth Potential:

1. Expanding Market Opportunity: The global 3D printing market, projected to grow at a 21% CAGR, creates a favourable backdrop for Nano Dimension to scale its operations.

Its focus on advanced industries like aerospace and defence aligns with high-growth applications requiring precision and customization.

2. Steady Revenue Growth: Nano Dimension has grown revenue from $38M (2021) to $50M (2023), driven by increased adoption of its DragonFly printers and materials.

Swazers Charts TA Chart Idea for NNDM

Financial Resilience:

1. Strong Cash Position: With $80M in cash reserves and a current ratio of 4.0, Nano Dimension has sufficient liquidity to sustain operations and fund innovation without the immediate need for external financing.

2. Low Leverage: The company’s debt-to-equity ratio of 0.10 ensures financial flexibility, reducing risks tied to rising interest rates or debt servicing.

Risks and Challenges.

Persistent Financial Losses:

1. Profitability Concerns: Despite narrowing losses, Nano Dimension remains unprofitable, with net losses of $15M in 2023 and negative operating cash flow (-$10M). Achieving profitability may take 3-5 years, depending on adoption rates and scaling efficiency.

2. High Operating Costs: while declining, still accounts for 40% of revenue, reflecting the capital-intensive nature of its business. These costs weigh on near-term margins.

Execution Risks:

1. Slow Adoption Curve: The adoption of 3D printing for additive electronics is progressing slower than for general-purpose 3D printing, which could limit revenue growth in the short term.

2. Integration Challenges: Expansion into new verticals or partnerships requires seamless integration of hardware, software, and materials to maintain customer satisfaction.

Competitive Pressures:

1. Market Competition: Nano Dimension competes with larger, better-funded players like Stratasys, 3D Systems, and Materialise, which dominate the broader 3D printing market.

Larger competitors benefit from established client bases and economies of scale.

2. Pricing Pressure: Nano Dimension’s premium pricing for its proprietary technology may face resistance in price-sensitive markets, limiting its scalability.

Strategic Recommendations.

Watch for Breakout or Breakdown:

Monitor the stock’s symmetrical triangle pattern, with a breakout and close above $2.25 potentially targeting $2.50-$2.75.

For Long-Term Investors:

Focus on Strategic Catalysts: Accumulate shares on dips near $2.00, with a 3-5 year investment horizon targeting broader adoption of additive electronics in aerospace, defence, and IoT markets.

Keep an eye on milestones such as profitability, cash flow neutrality, and major client acquisitions.

Risk-Reward Profile.

“The First to Apply AI to Additive Manufacturing”

“With artificial intelligence, a production machine becomes more than just a printer, but a node in a self-learning, self-coordinating network.”

Final Assessment.

Nano Dimension Ltd. is a high-risk, high-reward investment opportunity that stands out for its proprietary technology and strong financial foundation. However, the company’s reliance on a nascent market and continued operating losses limit its appeal to risk-averse investors.

Investment Outlook:

1. Bullish Case: Nano Dimension’s strong cash reserves, improving gross margins, and growing revenue provide a solid foundation for future growth.

The adoption of additive electronics across industries like aerospace, defence, and IoT could unlock significant revenue streams, validating its niche strategy.

2. Bearish Case: The company’s persistent losses and slower-than-expected adoption of its technology present execution risks, making it vulnerable to larger, more established competitors

Further delays in achieving profitability could lead to shareholder dilution if additional funding is required.

Overall Sentiment.

Nano Dimension is an ideal candidate for speculative, growth-focused investors who are willing to tolerate high volatility and long-term uncertainty. While its strong cash reserves provide near-term stability, the company must overcome significant barriers to achieve sustained profitability and market leadership.

This company demonstrates robust financial stability, profitability, and growth potential. Strategic investments in emerging markets and technology, coupled with disciplined cost management, make it an attractive candidate for long-term portfolios. However, keep an eye on liquidity and competition to mitigate potential risks.

#TriFusionAI © 2024 Bob Smith and John Swarbrick Follow us on X @BobSmithMSc and @SwazersC Disclaimer: This report is for educational purposes only and does not constitute financial advice. Errors and omissions may be present.